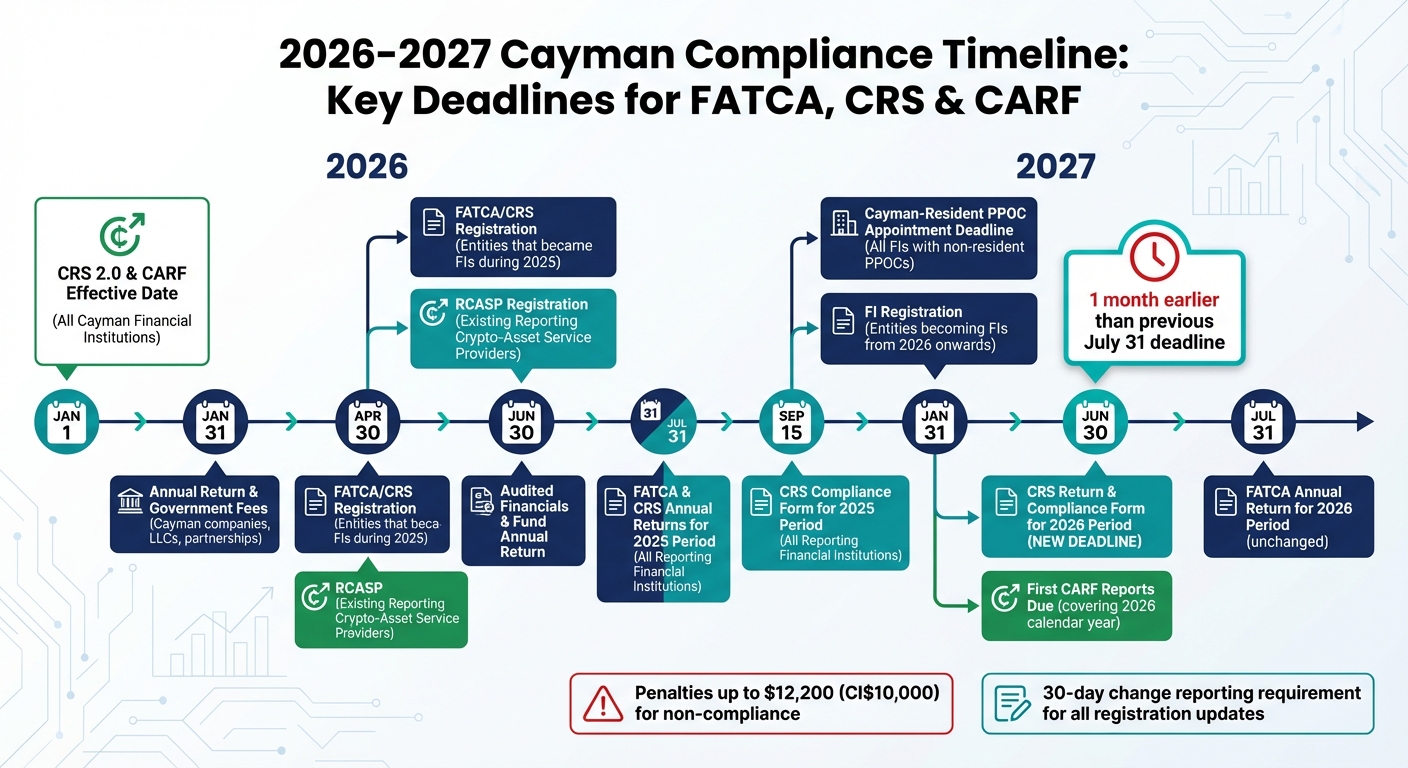

The Cayman Islands have introduced major updates to FATCA, CRS, and CARF regulations starting January 1, 2026. These changes impact reporting requirements for Cayman Islands hedge fund administration, especially those dealing with digital assets. Key updates include earlier deadlines, stricter penalties, and new compliance rules. Here’s what you need to know:

- CRS 2.0 & CARF: Expanded reporting now includes crypto-assets, electronic money, and CBDCs.

- New Deadlines: CRS filings for 2026 are due June 30, 2027, a month earlier than before. FATCA deadlines remain July 31.

- Local PPOC Mandate: All institutions must appoint a Cayman-based Principal Point of Contact by January 31, 2027.

- Stricter Penalties: Immediate fines up to $12,200 for non-compliance without prior notice.

- Enhanced Data Requirements: Institutions must report detailed account classifications and roles of Controlling Persons.

These updates emphasize accuracy, earlier compliance, and local accountability. Financial institutions must adjust internal processes and reporting systems to meet these new standards.

Cayman Islands FATCA, CRS, and CARF Compliance Deadlines 2026-2027

CRS Reporting Deadline Changes for 2026

June 30 Annual CRS Filing Deadline

Cayman’s regulatory framework is shifting its CRS filing deadlines, bringing earlier schedules for compliance. Starting with the 2026 reporting year (filings due in 2027), both the CRS Return and Compliance Form will need to be submitted by June 30, 2027. Previously, these deadlines were set for July 31 and September 15, respectively. Ogier highlights this change:

From the 2026 reporting year, the CRS Return filing deadline moves from 31 July 2027 to 30 June 2027.

For the 2025 reporting year (filings due in 2026), transitional rules remain in effect. The CRS Return deadline will still be July 31, 2026, and the Compliance Form deadline will remain September 15, 2026.

| Requirement | 2025 Reporting Year (Due 2026) | 2026 Reporting Year (Due 2027) |

|---|---|---|

| CRS Return Filing | July 31, 2026 | June 30, 2027 |

| CRS Compliance Form | September 15, 2026 | June 30, 2027 |

| FI Registration | April 30, 2026 | January 31, 2027 |

These adjustments significantly shorten the compliance window, adding new challenges for fund managers.

Effects of Earlier Filing Deadlines

The updated deadlines compress the preparation period, requiring faster adoption of compliance measures. The new schedule cuts the CRS Return preparation time by one month and shortens the Compliance Form timeline by 2.5 months. For fund managers, this means reworking internal processes to meet the tighter deadlines while ensuring data accuracy.

The condensed timeline also introduces stricter penalties for non-compliance. The Department for International Tax Cooperation (DITC) now has the authority to impose immediate administrative penalties of up to $12,200 (CI$10,000) per breach, without first issuing a notice of breach. Carey Olsen emphasizes the importance of preparation:

These changes require FIs to update their internal compliance calendars and ensure that all relevant information is prepared and submitted in a timely manner.

To adapt, financial institutions should consider implementing automated reminders for the June 30 deadline and strengthening internal controls and AI hedge fund administration to verify the accuracy and completeness of account data. These tighter deadlines are just one part of a broader push for stricter compliance across reporting, registration, and operational practices.

sbb-itb-9792f40

FATCA Filing Deadlines in 2026

July 31 FATCA Reporting Deadline Remains

The FATCA reporting deadlines for 2026 remain consistent. Financial institutions in the Cayman Islands must submit their FATCA annual returns by July 31, 2026, covering the 2025 reporting year. While CRS deadlines have shifted earlier, the FATCA timeline stays the same.

This schedule holds steady for the foreseeable future. For the 2027 filings, FATCA will still be due on July 31, while CRS moves to a June 30 deadline. This creates a one-month gap between the two reporting frameworks starting in 2027. Ogier highlights this distinction:

No changes have been made to FATCA registration and reporting deadlines (although Cayman Reporting Financial Institutions may wish to align their 2027 reporting under FATCA and CRS).

However, the unchanged FATCA deadline does not imply leniency in enforcement. The Tax Information Authority (TIA) now has the power to impose immediate penalties of $5,000 or $10,000 for late submissions, without issuing prior breach notices. Financial institutions are required to ensure their FATCA filings are "adequate, accurate and current", capturing all necessary details and updates in circumstances. Even if reporting tasks are delegated to third-party administrators, the financial institution remains accountable for compliance. This steady FATCA schedule contrasts with the evolving CRS requirements, prompting some institutions to explore unified reporting strategies.

Aligning FATCA and CRS Compliance Processes

With CRS deadlines moving earlier, many institutions are considering ways to streamline their reporting schedules. The separate deadlines for FATCA and CRS require financial institutions to manage two distinct reporting cycles. By aligning FATCA reporting with the June 30 CRS deadline starting in 2027, institutions can simplify their compliance efforts.

This approach has clear advantages. Consolidating both reporting obligations into a single compliance window minimizes resource strain and reduces the likelihood of missing the FATCA deadline due to competing priorities in July. It also allows institutions to focus their efforts more effectively.

To adopt this strategy, institutions should update their internal compliance calendars now, targeting a June 30 deadline for both FATCA and CRS starting in 2027. Additionally, they should establish clear protocols for submitting change notices on the DITC portal within 30 days of any updates to their classification, contact details, or service providers. Delays in these notices can result in automatic penalties of approximately $12,200 (CI$10,000). Financial institutions should also implement documented oversight measures, such as board resolutions or periodic reports, to monitor external service providers, as ultimate compliance responsibility always lies with the institution itself.

Ensuring FATCA and CRS Compliance – Updates and solutions for the latest enforcement guidelines

Updated Registration and Reporting Rules

Cayman financial institutions now face updated registration and reporting requirements, designed to streamline compliance and ensure timely filings.

January 31, 2026 FI Registration Deadline

To align with stricter filing schedules, new rules standardize registration deadlines. Cayman financial institutions established in 2025 must register with the TIA by April 30, 2026. For those becoming FIs from 2026 onward, the registration deadline is January 31 of the following year.

The registration form must include essential details such as the FI’s name, regulator-assigned numbers (like those from the General Registry or CIMA), CRS classification, and the date the entity became an FI.

| FI Category | Registration Deadline Date |

|---|---|

| Entities that became FIs in 2025 | April 30, 2026 |

| Entities becoming FIs from 2026 onwards | January 31 (following year) |

| Existing FIs with non-resident PPOCs | January 31, 2027 (PPOC update) |

All filings must include a declaration confirming that the information provided is "adequate, accurate, and current", reflecting any updates during the reporting period.

Cayman-Resident PPOC Requirement

A key change is the requirement for all reporting FIs to appoint a Principal Point of Contact (PPOC) who resides in the Cayman Islands. As explained by Loeb Smith Attorneys:

"The Amendment Regulations require the principal point of contact for each Cayman Financial Institution (‘PPOC’) to be located within the Cayman Islands. Previously, the PPOC could be based anywhere."

Existing FIs with non-resident PPOCs must appoint a Cayman-based PPOC by January 31, 2027 and notify the TIA via a change form. Institutions starting operations in 2025 but not registered by January 1, 2026, must register and designate a local PPOC by April 30, 2026.

This shift emphasizes local accountability, requiring boards and senior management to reassess how they manage CRS risks and controls. Failure to appoint a Cayman-resident PPOC can result in penalties of $12,200 (CI$10,000). Institutions without a Cayman presence may need to engage a local service provider to fulfill this role.

30-Day Change Reporting Requirement

Cayman financial institutions are also required to keep their registration information up to date under the new rules. Any changes to registration details – such as the FI’s name, contact information, CRS classification, PPOC, Authorizing Person, or service providers – must be reported via the DITC portal within 30 days.

Ogier provides further clarification:

"Where any information in an FI’s registration changes (for example, FI classification, contact details, PPoC, Authorising Person, service provider), the FI must file a change notice within 30 days of the change occurring."

To meet this requirement, FIs must implement robust controls to monitor internal changes and ensure timely updates on the DITC Portal. Failure to comply could lead to penalties, underscoring the importance of proactive management.

Additional CRS Reporting Data Fields

With the updated rules in place, financial institutions (FIs) in the Cayman Islands are now required to collect and report more detailed information under CRS 2.0. These updates, which align with the OECD‘s CRS 2.0 framework, enhance data collection standards and extend the scope to include digital assets.

Required Information Fields

Starting with the 2026 reporting year, FIs must report several new data points for each account. For instance, account classification must now specify whether an account is "new" or "pre-existing". Additionally, the joint account status must indicate if the account is held individually or jointly, along with the number of joint holders.

Another key change involves reporting the roles of Controlling Persons, such as settlor, trustee, protector, or beneficiary. For Investment Entities structured as trusts or partnerships, the roles of equity interest holders must also be disclosed.

FIs are now required to confirm the presence of valid self-certifications for all account holders. The definition of "Financial Assets" has been broadened to include "Relevant Crypto-Assets", while "Depository Accounts" now cover "Specified Electronic Money Products" and Central Bank Digital Currencies (CBDCs).

All reports must include a declaration that the submitted information is "adequate, accurate and current". As noted by the Maples Group:

"The amendments aim to strengthen data quality (requiring information to be ‘adequate, accurate and current’), harmonise due diligence with evolving anti-money laundering standards… and modernise definitions to explicitly capture crypto-assets."

For pre-existing accounts, these enhanced requirements are subject to transitional relief measures.

Transitional Period Through 2028

Acknowledging the operational challenges posed by these changes, transitional relief has been introduced for pre-existing accounts. For accounts maintained as of December 31, 2025, the requirement to report specific roles of Controlling Persons or equity interest holders applies only if the information is already stored in an electronically searchable format. This relief extends through the 2027 reporting period, with filings due by June 30, 2028.

Loeb Smith Attorneys explains the scope of this relief:

"For accounts maintained as at 31 December 2025, and for reporting periods ending by the second calendar year after that date, the additional information on roles is required only where that information already exists in electronically searchable form."

FIs must immediately review their electronic records to identify which Controlling Person roles are stored in searchable formats. This review will determine what data must be reported during the 2026–2027 transitional period. For accounts opened on or after January 1, 2026, all new data fields must be collected at or before account opening, with very limited exceptions.

To comply with these expanded requirements, funds need to update onboarding processes, revise self-certification forms using the latest templates from the Department for International Tax Cooperation (DITC), and upgrade IT systems to capture and store the additional data points. Entities involved in e-money, digital wallets, or crypto-custody must also reassess their classification, as they may now fall under the updated definitions of "Investment Entity" or "Depository Institution".

CARF Adoption for Crypto Funds

The Cayman Islands have taken a significant step in updating their financial transparency measures by introducing the Crypto-Asset Reporting Framework (CARF). This system, developed by the OECD, aims to improve tax reporting for crypto transactions and will take effect on January 1, 2026. Unlike the Common Reporting Standard (CRS), which focuses on account balances, CARF emphasizes transaction-based reporting. This includes exchanges between crypto-assets and fiat currencies, trades between different crypto-assets, and certain transfers. The framework specifically targets crypto service providers, as outlined below.

RCASP Registration and Reporting

CARF applies to Reporting Crypto-Asset Service Providers (RCASPs). These are entities or individuals based in the Cayman Islands that offer exchange services involving "Relevant Crypto-Assets" on behalf of their customers. Most Cayman investment funds that trade crypto-assets for their own accounts are excluded. However, funds or affiliated entities operating OTC desks or trading platforms may fall under CARF’s scope .

Existing RCASPs must register with the Tax Information Authority (TIA) through the DITC Portal by April 30, 2026. Newly established RCASPs must register by January 31 of the year following their launch. Additionally, RCASPs must comply with the local Proceeds of Crime (PPOC) requirements as part of the registration process .

Starting January 1, 2026, RCASPs must adopt a strict "No Cert, No Service" policy for new users. This means trading or account activation will not be allowed until the necessary self-certification is obtained. For users with accounts opened before December 31, 2025, RCASPs have a 12-month period from the go-live date to collect the required self-certifications.

CARF Requirements for Cayman Crypto Funds

CARF introduces specific reporting standards for crypto funds. The first reports, covering the 2026 calendar year, are due by June 30, 2027. Reportable transactions include retail payment transfers involving Relevant Crypto-Assets that exceed $50,000. Non-compliance carries hefty penalties: primary breaches can result in fines up to CI$50,000 (approximately $60,976), while missed filing deadlines can incur immediate penalties of $5,000 or $10,000 .

To streamline reporting, the amended CRS includes a coordination rule that exempts financial institutions from reporting gross proceeds already disclosed under CARF. Crypto funds must update their onboarding processes to capture all required self-certification details, ensure group affiliates are properly registered as RCASPs, and retain all CARF-related records for at least six years.

2026 Compliance Timeline

Cayman financial institutions face several critical deadlines in 2026 for CRS, FATCA, and CARF compliance, with penalties for non-compliance reaching up to $60,976 (CI$50,000).

Important Dates and Deadlines

The compliance journey begins on January 1, 2026, with the effective date of the Amended CRS and CARF, introducing new obligations. Financial institutions that started operations in 2025 must register by April 30, 2026, while those becoming financial institutions in 2026 have until January 31, 2027, under the updated permanent timeline. Additionally, Reporting Crypto-Asset Service Providers (RCASPs) already in operation need to complete registration via the DITC Portal by April 30, 2026.

For the 2025 reporting year, FATCA and CRS annual returns must be submitted by July 31, 2026, with the CRS Compliance Form due by September 15, 2026. Beginning with the 2026 reporting year (filed in 2027), the deadlines for both the CRS Return and CRS Compliance Form will shift to June 30, while FATCA returns will continue to be due on July 31.

Here’s a breakdown of the key 2026 deadlines:

| 2026 Date | Obligation | Applicable Entities |

|---|---|---|

| January 1 | Amended CRS & CARF Effective Date | All Cayman Financial Institutions |

| January 31 | Annual Return & Government Fees | Cayman companies, LLCs, and partnerships |

| April 30 | FATCA/CRS Registration | Entities that became FIs during 2025 |

| April 30 | RCASP Registration | Existing Reporting Crypto-Asset Service Providers |

| June 30 | Audited Financials & Fund Annual Return | CIMA-registered funds (Dec 31 FYE) |

| July 31 | FATCA & CRS Annual Returns (2025 Period) | All Reporting Financial Institutions |

| September 15 | CRS Compliance Form (2025 Period) | All Reporting Financial Institutions |

Strict compliance with these timelines is essential. Any changes to registration details must be reported to the DITC within 30 days to avoid a penalty of $12,200 (CI$10,000). Furthermore, entities must ensure they have a Cayman-based Principal Point of Contact (PPOC) by January 31, 2027.

Charter Group Fund Administration: Compliance Support for 2026

Navigating the compliance changes for 2026 requires expertise, and Charter Group Fund Administration offers essential support for Cayman-based funds adapting to the updated FATCA, CRS, and CARF regulations. The firm provides consistent updates on CRS and FATCA obligations while guiding funds to key resources, including template self-certification forms from the Cayman Islands Department for International Tax Cooperation (DITC).

Charter Group simplifies the shift to CRS 2.0, addressing the complexities introduced by the 2026 amendments. This includes capturing detailed data, such as the roles of Controlling Persons and account statuses, ensuring compliance with the "adequate, accurate, and current" declaration standards outlined in the 2025 Amendment Regulations. Their advanced reporting tools help funds meet these updated requirements seamlessly.

For funds dealing with digital assets, Charter Group offers specialized advice on valuing crypto-assets under the expanded CRS definitions. They also assist in determining whether digital asset activities fall under the revised CRS framework or the new Crypto-Asset Reporting Framework (CARF).

Beyond advisory services, Charter Group handles practical regulatory obligations. They help funds comply with the Cayman-resident Principal Point of Contact (PPOC) requirement by January 31, 2027, and adjust internal reporting schedules to meet the accelerated June 30 deadline for CRS returns and compliance forms starting in 2026. Additionally, the firm manages the ongoing 30-day notification requirement for updating financial institution registration details via the DITC Portal. This operational support ensures funds stay fully compliant with all new filing mandates.

Conclusion

Starting January 1, 2026, the Cayman Islands has rolled out CRS 2.0 and the Crypto-Asset Reporting Framework (CARF), bringing digital assets into the reporting fold while tightening certain deadlines. Notably, CRS filings for the 2026 reporting period are due by June 30, and FATCA filings maintain their July 31 deadline.

Cayman financial institutions now face new obligations, including appointing a Cayman-resident Principal Point of Contact by January 31, 2027, and making registration updates within 30 days. Enhanced data quality standards require a declaration that submitted information is "adequate, accurate, and current", along with new data fields like joint account statuses and Controlling Person roles. Penalties for non-compliance can reach up to $12,200.

Enforcement measures are also more stringent. As highlighted by Carey Olsen:

The DITC will have the power to impose immediate penalties of $5,000 or $10,000 for missed filing deadlines, without first issuing a breach notice.

To navigate these changes, expert guidance is more important than ever. Charter Group Fund Administration offers tailored solutions to help funds meet the demands of the updated regulatory framework. These services include managing accelerated filing timelines, ensuring high data quality standards, addressing Cayman-resident PPOC requirements, and tackling crypto-asset reporting obligations.

FAQs

Does my fund become a Reporting FI under CRS 2.0?

If your fund meets the definition of a Financial Institution, it could be classified as a Reporting Financial Institution (FI) under CRS 2.0. This classification comes with updated reporting obligations, including an expanded list of reportable assets and additional compliance standards, which take effect on January 1, 2026. It’s crucial to carefully examine the updated scope and registration criteria to understand your fund’s responsibilities and ensure compliance.

What steps are needed to meet the Cayman-resident PPOC rule?

Financial Institutions operating in the Cayman Islands must adhere to the requirement of appointing a Principal Point of Contact (PPOC) who resides locally. Notifications to the Tax Information Authority (TIA) are time-sensitive:

- If registered before January 1, 2026, the deadline is January 31, 2027.

- If activities began in 2025 without prior registration, the notification must be submitted by April 30, 2026.

Will our crypto activity trigger CARF reporting as an RCASP?

If you’re involved in crypto activities like providing exchange services or running platforms that facilitate transactions in specific crypto-assets, you might fall under CARF reporting requirements. The Crypto-Asset Reporting Framework (CARF) applies to Cayman Reporting Crypto-Asset Service Providers (RCASPs) engaged in exchange transactions. To stay compliant, take a close look at your operations and assess whether they align with these reporting obligations.